The ICC has recently released its 2025 Dispute Resolution Statistics Report. Daniel Wilmot and James Coen consider some of the key themes revealed in the analysis.

The report covers the calendar year 2025, in which 881 arbitrations were filed under the ICC Arbitration Rules. By the close of that year, 1,869 cases were pending before the ICC: a record number in which an aggregate value of $299bn was in dispute (falling from $354bn in 2024).

It examines caseload types (including regions, dispute types and value), the makeup of parties and tribunals, seats of arbitration and choices of law, and key data on the types and number of awards rendered. It also analyses the ICC’s expedited and emergency arbitration procedures, as well as the ICC’s other alternative dispute resolution services.

Some interesting observations can be drawn from the data:

- Case load and value remain very high comparatively, but the gap between the ICC and its competitors is narrowing in some respects.

- For example, the aggregate value being handled by SIAC in 2025 ($53bn) is dwarfed by the ICC’s same datapoint. That said, SIAC received 886 new arbitral references in 2025, beating the ICC by five, and the American Arbitration Association has reported 725 international arbitrations in 2025. By contrast, the LCIA’s most recent casework report (for 2024) shows 318 new arbitrations (still well below the 2020 peak of 407), and the SCC has reported 213 new cases for 2025. There is a significant divergence in the number of cases handled by the leading institutions.

- What is certain is that rival institutions will continue to try to compete with the ICC in the immediate and longer term, albeit they will need to work hard: the number of parties registered in ICC arbitrations last year was 2,531, the highest since the COVID-19 year of 2020 (2,507).

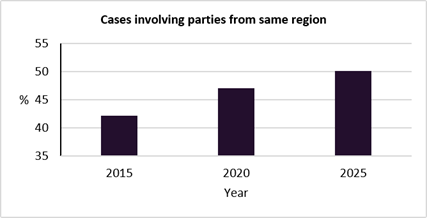

- ICC arbitration remains cross-border in the majority of disputes it handles (69.4%). But the data also indicates that it may be becoming more regional over time, suggesting that this forum increasingly serves domestic supply chains and investment relationships with immediate neighbours, over purely inter-continental ones:

- Europe continues to dominate in some ways, but not in others, and arguably ICC arbitration’s future growth lies outside that region and outside the Anglosphere:

- The UK leads the way in the nationality of confirmed/appointed arbitrators (10.89%), perhaps reflecting the fact that English law remains the most popular choice of governing law for parties (13% of 2025’s new cases are English law disputes). Paris remains the most frequently selected seat for ICC arbitration, but only just beating London (12% against 11.5%). More generally, 48.3% of the ICC’s 2025 arbitrations are seated in Europe, well ahead of the second most-frequently selected location (the USA at 11.6%). And, in aggregate, North & West Europe is the region where the most parties are from (28.8%).

- Against that, parties from the USA are the most frequently-represented (11.22%), with Brazil in second place (212 – 8.38%, a record). Record participation has been achieved in key jurisdictions, including China (102 parties) and Australia (34). As a region, albeit North & West Europe leads, Latin America and the Caribbean are second in terms of origin of parties (19.5%), and East and South Asia & Pacific is third (13.9%), ahead of North America (12.6%). So, Europe as a whole does not dominate completely (Central and South-East Europe as a region comes sixth out of eight).

- The Middle East represented 10% of the overall party population in 2025. This is possibly explained by the fact that construction and energy disputes continue to dominate the ICC’s case load, comprising 43% of new cases in 2025. The reality continues to be that ICC arbitration remains fundamentally linked to well-established capital investment construction and infrastructure projects and their disputes.

- Brazil presents a notable case. As well as being the second most frequently represented origin for parties, it also registered the most “domestic” ICC arbitrations in 2025 (i.e., arbitration where all parties are from the same place). This has had a knock-on effect on other data points: Brazilian arbitrators are the third most represented (7%), the country was in the top 10 for seats (37), and its law was chosen in 54 cases (third behind the UK and the laws of the USA). An exceptional case that leads to exceptional data – but perhaps a sign of things to come given Brazil’s influence in the Latin American region.

- Emergency Arbitration applications have jumped by 76% in one year (from 17 to 30). While less dramatic, the application of the expedited arbitration procedure has also increased (by 11%, from 152 to 169). All told, the mechanisms provided by the ICC to complement traditional arbitration are becoming embedded, and it will be interesting to see how the Highly Expedited Arbitration procedure newly introduced under the 2026 Arbitration Rules fares.

- North & West Europe remains dominant when it comes to the sourcing of arbitrators: 45.3% of arbitrators are from that region, and confirmations/appointments from some regions (for example, Sub-Saharan Africa, North Africa) seem strikingly low (respectively, 2.7% and 2.6 %).

- Women also remain underrepresented as arbitrators: in 2025, only 29.6% of arbitrator appointments/confirmations were female. The data seems to suggest that parties are worst at nominating women as arbitrators: of all the party nominations made in 2025, only 23% were of women. Although only marginally better, tribunal wing members seem similarly to struggle to appoint women to chair tribunals: of the cases where the chairperson is nominated by the co-arbitrators, only 30% were women. There will always be case-specific nuances, but parties and co-arbitrators need to be braver in nominating female arbitrators. The ICC Court leads the way in this regard – of the arbitrators it appointed in 2025, in 44.6% of cases women were appointed. Laudable of course, but these efforts alone cannot rectify the situation.

- Arbitrators are making more disclosures than in previous years: in 2025, 41% of arbitrators made disclosures before their appointment/confirmation (that figure was 30% in 2020).

- The ICC encourages disclosures and notes that they do not imply a conflict. That might feed into the outcomes of challenges to appointments made in 2025: of the 38 made (in 29 cases), only two were accepted by the ICC Court.

- It will be interesting to see how this data changes in future years in light of the new Article 12(2) in the 2026 Arbitration Rules (which mandates that doubts about a disclosure be resolved in favour of disclosure), as well as Article 12(3) (an arbitrator’s ongoing duty to disclose) and Article 12(5) (whereby parties must at the early pleadings stage provide a list of persons they believe will assist arbitrators (actual and prospective) to comply with their disclosure obligations).

- In the English jurisdiction, these new disclosure rules sit alongside the new and mandatory provisions of section 23A of the Arbitration Act 2025, which came into effect in August last year. With these two provisions now in force, it is easy to expect that there will be more challenges to arbitral appointments in London-seated ICC arbitrations: what is less clear is whether the success rate will increase in tandem.

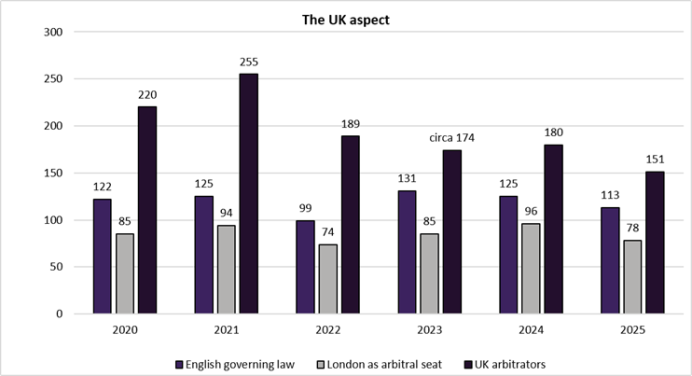

- And what of London? As noted above, in the ICC context, UK arbitrators remain the most frequently confirmed/appointed, and English law remains the most selected law by parties for their substantive disputes. In 2025, London was the second-most popular seat of ICC arbitration behind Paris. No other jurisdiction has such combined strength in these three areas in 2025, albeit it is worth comparing the data with previous years:

-

- While governing law choice and London as a venue have remained relatively stable over the past six years, there appears to be a downward trend when it comes to the appointment of UK-national arbitrators. It will be interesting to see how this develops in future years and to diagnose the causes: a reflection of the ever-growing globalisation of arbitration, the changing nationalities of the users of arbitration, or venue competition?

- This trend notwithstanding, the statistics seem to demonstrate (for now) the continued prominence of the ‘English’ jurisdiction in international arbitration, both for the respect that English law gives to the bargains parties strike in their commercial agreements (giving parties more certainty that their transactions will be respected on their own terms) and for the pro-arbitration policy of the English courts, where they are acting in a supervisory capacity.

- Will English law’s dominance in ICC commercial arbitration become less absolute in future? Perhaps. There are many factors that come into play in answering such question, including the usual suspects of cost and delay. What is clear is that English law’s certainty, fairness and swiftness (on substance and procedure) remains a key driver and that seems a factor that is unlikely to change soon.

- But it does seem to be the case that the determination of English law ICC cases will not be the exclusive preserve of UK-national arbitrators in future. Perhaps that expresses the global reach and attractiveness of English law as a qualifying discipline (e., perhaps more non-UK arbitrators are English-qualified lawyers). But it could also reflect the increased confidence of non-English qualified arbitrators from outside the UK (including non-lawyer arbitrators) in dealing with English law disputes.